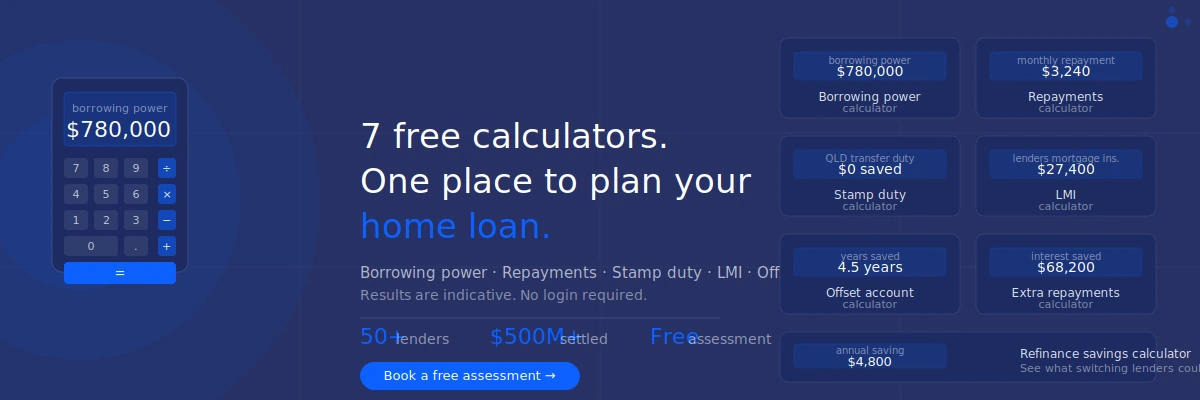

Whether you’re starting to plan your first home purchase or reviewing an existing loan, our free home loan calculators give you clear, instant estimates across the questions that matter most.

Every calculator on this page runs entirely in your browser. No login. No personal data required. And no obligation. When the numbers raise more questions than they answer, our brokers are here, just book a free assessment and we’ll work through the specifics with you.

Select the calculator that matches where you are in your home loan journey. Not sure which one to start with? If you’re buying your first home, start with Borrowing Power.

The first question anyone asks when they start thinking about a home loan. How much can I actually borrow? Our borrowing power calculator estimates your capacity based on your income, living expenses, existing debts, number of dependants, and the assessment rate lenders apply. Results show a conservative range, an estimated mid-point, and an optimistic figure based on income multiples.

Best for: First home buyers, anyone at the start of their planning journey, buyers who want to understand their budget before inspecting properties.

Defence Home Ownership Assistance Scheme (DHOAS) is one of the most underused benefits available to serving and eligible former Australian Defence Force members. Our DHOAS subsidy calculator estimates your monthly subsidy entitlement based on your service tier and loan balance, so you can see the real cost of your home loan after the government contribution is applied. Subsidy rates are set by DVA and reviewed annually, the calculator uses the current March 2026 rates.

Best for: ADF members, veterans, and their families who want to understand their DHOAS entitlement before applying for a home loan or refinancing an existing one.

The First Home Guarantee allows eligible first home buyers to purchase with as little as a 5% deposit without paying Lenders Mortgage Insurance. Our First Home Guarantee calculator shows your minimum deposit, estimated LMI saving, and how the scheme changes your upfront cost compared to buying outside the guarantee. It also flags whether stacking the guarantee with the Queensland First Home Owner Grant and stamp duty exemption applies to your situation.

Best for: First home buyers in Queensland weighing deposit strategies. Buyers who want to understand the full dollar impact of the scheme before speaking to a lender.

Once you know what you want to borrow, the next question is: what will the repayments actually be? Our repayment calculator works for any loan amount, interest rate, and term. You can model principal and interest or interest only, and see monthly versus fortnightly repayments side by side. It also shows your LVR and flags whether LMI may apply based on your deposit.

Best for: Buyers stress-testing whether a purchase is affordable at their target price. Also useful for investors modelling cash flow on an investment loan.

Transfer duty (stamp duty) in Queensland is one of the biggest upfront costs in a property purchase — but first home buyers can access significant concessions. Our Queensland stamp duty calculator calculates your exact duty based on purchase price, property type (new or established), and buyer type (first home buyer, investor, foreign purchaser). It also applies the current first home buyer concessions: zero duty on new homes and vacant land, and a full concession on established homes up to $709,999.

Best for: Anyone buying in Queensland who wants to know their full upfront cost before making an offer.

Lenders Mortgage Insurance is one of the most misunderstood costs in home buying. Our LMI calculator shows you exactly what LMI would cost at your purchase price and deposit level and immediately flags whether you could avoid it entirely through the First Home Guarantee or by adjusting your deposit. LMI on a $700,000 purchase with a 5% deposit can exceed $25,000. It is worth knowing the number before you commit to a deposit strategy.

Best for: First home buyers weighing a smaller deposit against the LMI cost. Also useful for investors considering how LVR affects their structure.

Loan-to-Value Ratio is the single number that determines whether LMI applies, which lenders will consider your application, and what interest rate tier you qualify for. Our LVR calculator takes your property value and loan amount — or deposit — and immediately shows your LVR, whether you’re above or below the critical 80% threshold, and an indicative LMI position. It also works in reverse: enter your target LVR and it calculates the deposit you need.

Best for: Buyers working out how much deposit to save before making an offer. Existing borrowers checking whether they’ve crossed the 80% LVR threshold through repayments or property growth.

An offset account is one of the most effective tools available to Australian home loan borrowers but most people don’t realise how powerful it is until they see the numbers. Our offset account calculator shows how much interest you could save and how many years you could reduce from your loan term simply by keeping your savings in an offset account rather than a separate savings account.

Best for: Existing borrowers reviewing their loan structure. Buyers deciding whether a loan with an offset account is worth a slightly higher rate.

Making even modest additional repayments can cut years from your loan and save tens of thousands in interest. Our extra repayments calculator lets you model the impact of any additional monthly amount to see the time saved and interest avoided over the life of the loan.

Best for: Borrowers who have recently received a pay rise, bonus, or inheritance and want to understand the best use of additional funds.

If you haven’t reviewed your home loan in the last two years, there is a reasonable chance you’re paying a rate that’s no longer competitive. Our refinance savings calculator compares your current loan to a lower rate and shows your monthly savings, annual savings, and total interest saved over the remaining loan term. It also shows your break-even point after switching costs.

Best for: Existing borrowers on a rate that hasn’t been reviewed recently. Anyone considering whether refinancing is worth the effort and cost.

Negative gearing reduces your taxable income by the amount your investment property costs exceed the rental income it generates but the real after-tax holding cost depends entirely on your marginal tax rate and whether you include depreciation. Our negative gearing calculator models your property’s annual shortfall, the tax deduction it generates at your bracket, the impact of Div 43 building depreciation and Div 40 plant depreciation, and your PAYG withholding variation estimate all in a single view.

Best for: Investors evaluating an investment property’s real weekly cost after tax. Anyone who wants to understand whether a PAYG variation is worth applying for before the next financial year.

Rental yield is the primary metric for comparing investment properties, but gross yield and net yield tell very different stories. Our rental yield calculator calculates both: gross yield from purchase price and weekly rent, and net yield after factoring in council rates, property management fees, insurance, maintenance, and vacancy. It also shows the yield on your actual cash invested rather than the purchase price — which is the number that matters most for equity-funded purchases.

Best for: Investors comparing multiple properties or markets. Anyone assessing whether a property’s rental income is sufficient relative to its holding costs before committing to a purchase.

Every calculator on this page uses standardised assumptions. They do not know your employer, your credit history, your property type, or which of our 50-plus lenders is most likely to approve your application at the best available rate.

The same borrower with the same income can receive materially different results from different lenders depending on how they assess overtime, rental income, self-employment, or business debt. A calculator treats all lenders the same. A broker does not.

At Stanford Financial, we use the numbers from tools like these as a starting point for the conversation — then we go deeper. We identify which lenders suit your profile, what rate you can realistically access, and how to structure your application to give you the strongest possible outcome.

A calculator gives you a range. A broker gives you a plan. Our team is based in Springfield Central and works with clients across Queensland and Australia wide. A free assessment takes around 30 minutes and will give you a clear picture of your borrowing capacity, the lenders most suited to your situation, and the steps to get from where you are to where you want to be.

Book your free assessment today. Call us on 0483 980 002 or contact us online.